A Data Strategy for GHGP Scope 3 Accounting and Reporting

Carbon accounting is a complex process to say the least. For businesses to learn the new processes, set measurement metrics and establish reporting capabilities for the GHCP and SEC, they are likely to hire a significant team and spend $677,000 per year on these tasks.

With this kind of money at stake and the 2024 reporting deadline looming, one of the greatest risks — and opportunities — resides in your data strategy. How you will acquire, store, harmonize and deliver these data to a climate accounting management platform (CMAP) or ESG reporting solution will make the difference between early success and failure with carbon accounting.

At HULFT, we estimate that a manufacturing company with $500 million in revenue will have approximately 130 sources of emissions-related data that come from at least 30 enterprise data systems that reside inside their company, at energy suppliers or at partner companies in the value chain. Just as challenging, these data will be delivered in a wide variety of formats.

Data Strategy Components

To produce financial-grade reports that are auditable, all data sources must have a well-understood lineage and how they are transformed into the final product. This requires confidence in the data and its audibility at every step in the process. Towards this end, I believe there are five components of an effective carbon data strategy:

- Data Definition – defining the categories and types of data you will need, who owns them and where they are located.

- Data Acquisition – determining how you will acquire the data – with humans, machines or both.

- Data Storage – deciding where it will reside after acquisition, be it a centralized data lake or in databases.

- Data Calculation – leveraging the industry standard requirement emissions factors and calculations.

- Reporting – for the SEC and other climate-oriented governing bodies.

Working with Scopes 1 and 2 data are relatively straightforward. They come from individual energy providers for electricity, steam, and HVAC inside the company. Today, you can often obtain a data feed from your utility providers via an online portal or an application programming interface (API). If that option is not available, there is also OCR scanning of PDF files, and other ways to turn analog to digital.

If you have the resources, there are several ESG software and service companies such as WatchWire, which automatically acquires utility invoices from providers so you no longer need to manually extract data from utilities. These solutions are not cheap but they help ensure data accuracy and provide advanced analytics for reporting and can eventually make future predictions on electric, steam, natural gas, and water consumption based on historical invoice data.

Scope 3 Data Challenges

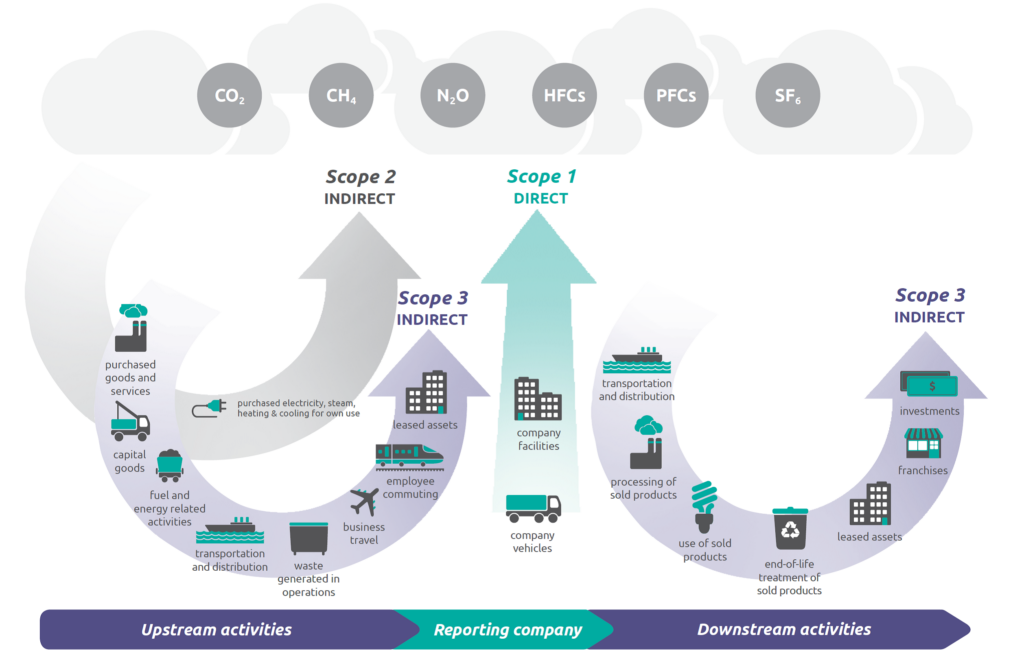

As we all know by now, the greatest complexities in climate accounting reside in Scope 3 data. On the upstream side of the business, this includes, but is not limited to: leased assets, employee commute, transportation and distribution, waste generated during operations, fuel and energy-related activities, business travel, capital goods, purchased goods and services. On the downstream side, this includes the processing of sold products, transportation and distribution, use of sold products, end-of-life sold product treatment, franchises, and investments (See the EPA diagram)

With much of Scope 1 and 2 data, the location, quality and format are known. With Scope 3, the data dimensions are harder to understand, and it requires one or more partners outside of your control to manage each data source. This adds the following additional complexities:

- Manual data gathering processes

- Humans sometimes delivering data instead of machines

- Lack of access – aka ‘siloed’ data

- Expenses related to data acquisition – hard costs and staff time are nontrivial

- You don’t understand what is being collected and why

- Lack of partner and stakeholder engagement and communication

- Limited budgets

- Non-standard business processes that result in low quality

Ensuring Data Quality

The data required to calculate GHG emissions is often scattered across various internal systems throughout the organization. Many of these systems may be incompatible and don’t ‘talk’ to each other. Or the utility suppliers might not have systems and processes in place to share data. To ensure a complete and accurate data foundation to underpin your reporting and decarbonization efforts, your team needs to determine how to source data on an ongoing basis. Some suggestions on this front include:

- Consider outsourcing the data capture process to a specialist service provider

- Get as close to the original data source as you can. If you have a choice between meter or billing data, use meter data

- Aim for automated data transfer wherever possible. Minimize human intervention: files touched by people prior to data collection are more prone to failure to load, precision loss and metric confusion

- Consider how you will store and manage the data on an ongoing basis. A cloud-based enterprise software platform is infinitely superior to spreadsheets for this task

Even though carbon accounting is a new practice in the business world, there are several technology developments that occurred over the past two decades including Enterprise Resource Planning, Customer Relationship Management and Ecommerce that provide sound and similar frameworks that can be leveraged for carbon accounting. In the end, carbon accounting is the combination of people, data, business processes and technology to achieve a measurable outcome. By leveraging already-established frameworks and engaging with the teams inside your company that have completed large-scale technology initiatives, you are well on your way towards your first carbon emissions report in 2024 or soon after.